Q1 2016 Client Letter

April 2016

If you look at markets only once a quarter, the first three months of 2016 appear relatively uneventful, at least on the surface. The S&P 500 was up 1.4%, U.S. small cap stocks were down -1.5%, and the Barclays U.S. Aggregate Bond Index was up 3.0% on the year. Developed international equities were down -3.0% but emerging market equities were up 5.7%.

For those of us who follow markets more closely, it was anything but boring. The final numbers mask the underlying uncertainty and volatility that played out in the quarter. The S&P 500 declined more than 10% in the first six weeks of the year – the worst calendar year start in its history. The downward pressure was fueled by the usual suspects: concern over global economic growth, particularly in China; continued weakness in the price of oil and other industrial commodities; monetary policy uncertainty and fear of rising interest rates in the U.S.; and disappointing prospects for corporate revenues and earnings.

Sentiment improved and markets changed course in the middle of February. There was talk of a potential deal among OPEC countries to cap oil production and address the return of Iran to the global supply chain. The Federal Reserve was more dovish in their comments and reduced the number of expected 2016 rate hikes from four to two. The European Central Bank announced a more aggressive stimulus plan to cut interest rates and increase the size of their quantitative easing program, including a program to purchase corporate bonds. Equity markets responded positively to these developments. After its dreadful start to the year, the S&P 500 enjoyed one of its best ever advances for the month of March. Developed international and emerging market equities also advanced, as did crude oil. By the end of the quarter the S&P 500 returned to positive territory for a quarterly performance that was “turbulently flatâ€.

Despite the drama and volatility, there was little change in the underlying fundamentals that ultimately drive long-term investment performance, such as sales revenues, profit margins, and corporate earnings. In fact the past year has seen a growing divergence between security prices and their underlying fundamentals. For example, while the market is only 3% below its all-time-high, some analysts are expecting S&P 500 earnings to decline by more than 9% in the first quarter of 2016. This would be the largest decline in earnings since 2009, and the fourth consecutive quarter with a decline in earnings.

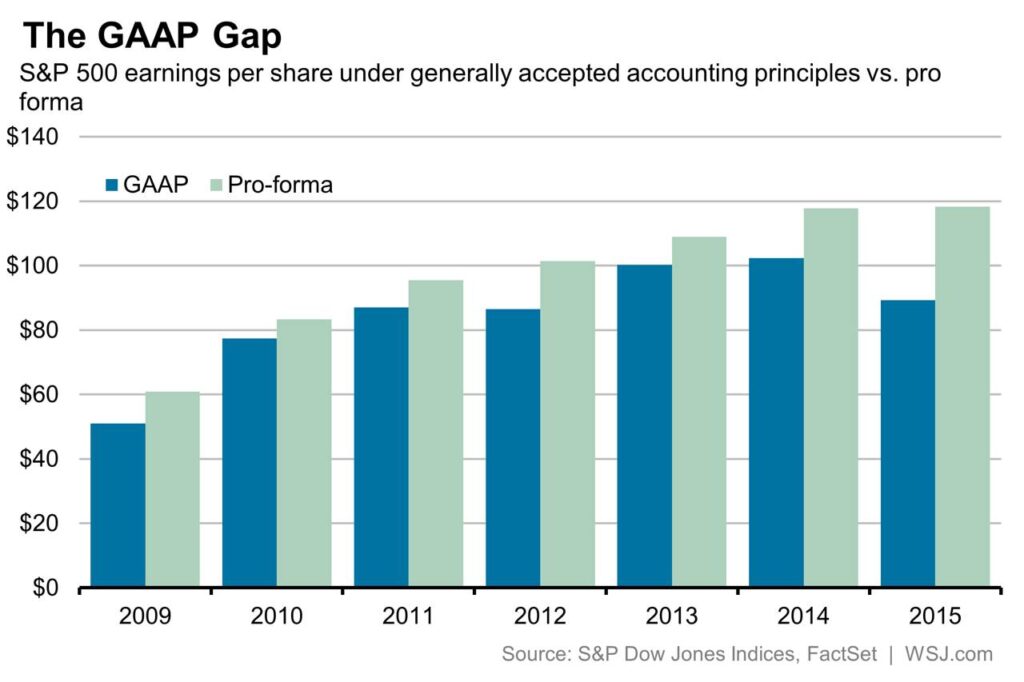

Furthermore, the quality of the reported earnings has come into question. There is an increasing separation between GAAP earnings (Generally Accepted Accounting Principles), and Pro-forma earnings (earnings excluding extraordinary or supposedly “one-time†items). Warren Buffett commented on this phenomenon in his most recent letter to Berkshire Hathaway shareholders in typically blunt terms:

“It has become common for managers to tell their owners to ignore certain expense items that are all too real. ‘Stock-based compensation’ is the most egregious example. The very name says it all: ‘compensation.’ If compensation isn’t an expense, what is it? And, if real and recurring expenses don’t belong in the calculation of earnings, where in the world do they belong?â€

With organic sales and revenue growth difficult to find, companies are increasingly turning to financial engineering tactics to boost their numbers. Low cost borrowing has fueled merger and acquisition activity and share buybacks. Pro-forma earnings are increasingly emphasized and may obscure actual performance. These activities are a response to stubbornly sluggish fundamentals.

Looking forward, we would expect these divergences to be resolved over time in one of three ways: improving fundamentals rise to meet the market, the market falls to meet sluggish fundamentals, or some combination thereof.

While most might prefer the first option, we consider the latter to be more likely. Under the third option, we would expect continued volatility as the market moves sideways in a range-bound manner while prices and fundamentals gradually converge. Earnings season has begun and we will be watching closely for signs of improving fundamentals and pockets of opportunity.

In challenging times like these it is important to maintain a long-term strategic perspective. In an effort to add value over the long haul, we continue to dedicate energy to finding investment opportunities in less-trafficked areas that function independently of the public markets. We remain committed to the thoughtful and diligent process that has served our client families well over the years.

On administrative matters, please find enclosed our privacy policy and a summary of the Material Changes to our ADV Brochure filed on March 25th, 2016. Please let us know if you would like a copy of the full Brochure. Please also let us know promptly of any significant change in your financial circumstances that would necessitate revisiting your investment objectives or re-evaluating the management of your assets.

As always, we welcome your thoughts and appreciate the confidence you have placed in our firm. We are grateful for the opportunity to work with you and your family.

Nichoals Hoffman & Co.